The CEO of a Norwegian hardware startup shared with me his pitch deck, which included some unusual slides. It included the company's capitalization table, a breakdown of who owned what part of the company. Cap tables are typically shared during the investment diligence stage.

If you take a closer look at the table, something is very wrong.

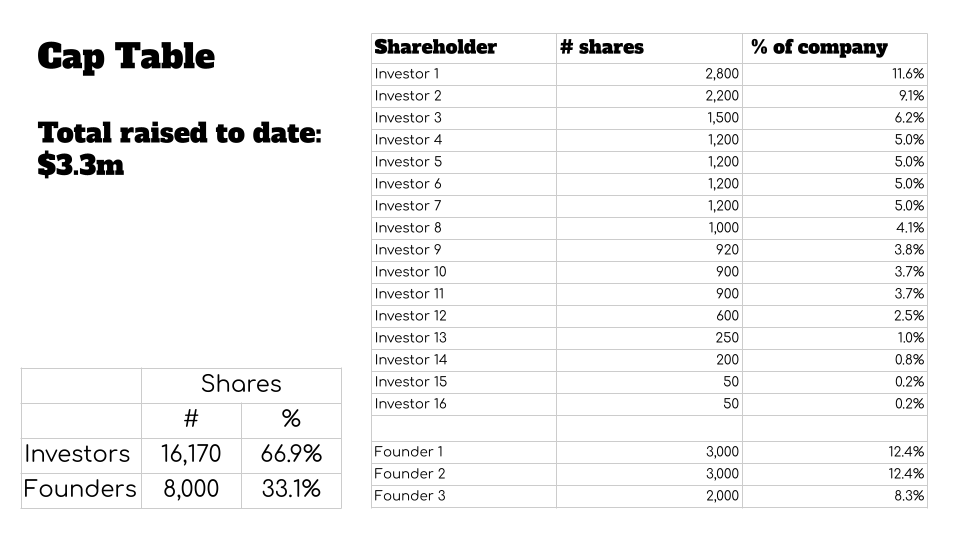

This cap chart is an exact reproduction of the cap chart that was in the deck. Condensed and edited to remove investor names. Image credit: Haje Kamps/TechCrunch

The problem here is that the company gave up more than two-thirds of its equity to raise $3.3 million. The company has launched a $5 million funding round, but this is a serious hurdle.

TechCrunch interviewed a number of Silicon Valley investors and hypothesized whether they would invest in a founder who presented a cap table with similar dynamics to the one shown above. What we learned is that while the current cap table makes the company essentially uninvestable, there's still hope.

Why is this such a big deal?

In less sophisticated startup ecosystems, investors can be tempted to make short-sighted decisions, such as trying to acquire a 30% stake in a company with a relatively small funding round. . To someone who isn't familiar with how startups work in the long term, that may seem like a sensible goal. Isn't it an investor's job to make as much money as possible for the money they invest? Perhaps that's true, but within that dynamic lies a virtual poison that limits a startup's growth. At some point, a company's founders have so little capital left that the cost-benefit analysis of the grueling death march of running a startup begins to weigh against them continuing to give it their all.

“There's one big red flag on this cap table: The investor base owns twice as much wealth as the three founders combined,” said Leslie Finezaig, general partner at Graham & Walker. ” he said. “I want our founders to be actively involved in the game.”

Feinzaig said the company is currently “essentially uninvestable” unless new leads come in and fix the cap table. Of course, that in itself is a risky move and will take a lot of time, energy, money, and lawyers.

“Fixing the cap table means packing in existing investors and returning ownership to the founders,” Feinzaig said. “This is an aggressive move, and I don’t think many new investors will want to go that far. If this is the next OpenAI, they will find a leader to help solve this problem. However, it is very difficult to stand out this clearly at the seed stage, much less in the current VC market.”

Having unmotivated founders can cause a company to exit sooner than it would otherwise. For those of us who live and breathe the venture capital business model, this is a bad sign. It leads to mediocre outcomes for startup founders, limits the amount of angel investment they can do, and makes entry-level funding impossible. Startup ecosystem.

Such an early exit would also limit VC's potential upside. If the company later exits at a much higher valuation, he stands a better chance of getting a huge 100x return on his one investment. This means that profits for limited partners (i.e. those who invest in VC firms) will be reduced. Over time, LPs get tired of it. The whole point of VC as an asset class is that it's incredibly risky, with the potential for incredibly high returns. When LPs go elsewhere for high-risk investments, the entire startup ecosystem collapses due to lack of funds.

There are potential solutions

“We want to try to make the seeding and Series A cap tables look 'normal,'” Homebrew general partner Hunter Walk told TechCrunch. “Typically, the investors own a minority of the overall company, the founders still have sound ownership and are invested in it, and the company/team/pool has the rest of the common equity.” [stock]”

I asked the CEO and founder of the hardware company in question how the company got into this mess. He requested anonymity so as not to jeopardize the company or put investors at a disadvantage. He explained that the team had a lot of experience in large companies, but lacked experience in the startup world. In other words, we didn't know how much work it would take to bring the product to market. He said internally that the company would accept terms “for this round only” and would seek a higher valuation in the next round. Of course, as the company continued to face delays and problems, investors traded wildly and were faced with a choice between running out of money or taking a bad deal, and the company decided to take the bad deal.

The CEO said the company is building solutions to problems experienced by 1.7 billion people and has a new patent-pending product that has been successfully tested for six months. At first glance, it looks like a company with billion-dollar potential.

The current plan is for the company to raise $5 million in the current round and then try to fix the cap table. That's a good idea in theory, but the startup has ambitions to raise money from overseas investors who will have input on the cap table itself. And that may raise questions about the founders themselves.

Cleaning up the cap table

“A situation like this that merits a ‘clean-up’ certainly does not automatically result in a ‘pass,’ but it does require the company and the cap table to undertake some degree of restructuring to correct the incentive structure in parallel with raising capital.” We need to accept it,” Wolk said. “If we feel that a settlement is nearly impossible (even if we play the ‘bad guy’ on behalf of the founder), we often advise CEOs to settle before raising further capital. ”

Mary Grove of Bread & Butter Ventures says that when founders own very little equity in their company at the seed stage, it's especially true that some of the equity is not paid to key hires and investors I agree that owning the remaining 66% is a red flag.

“We want to understand the reasoning behind why the company did so much dilution at such an early stage. “Maybe it's because some early investors or bad actors who had no experience in dealing with venture capital took advantage of that,” Grove told TechCrunch. “Or is there an underlying reason why the business has become so difficult to raise capital (look at revenue growth, churn rates, etc.)? (Was there any litigation or other issues?))? Depending on the reason, if the business and team meet our investment filters and we believe it's the right partnership, we may be delayed in finding our way forward. ”

Grove said Bread and Butter ventures want the founders to own a combined 50-75% stake at this stage of the company, the opposite of what is seen in the reproduction above. He stated that this would ensure that interests were aligned and that the founders would be evaluated. Incentives for venture-backed companies to build for the future. She suggests that her company may have a term sheet that includes corrective actions.

“Before we lead or invest in a new round, we ask the founders to receive additional option grants to bring their combined ownership to 50-75%,” Grove said. , she points out the challenges in this regard as follows: This means existing investors on the cap table will also participate in the overall dilution to achieve this reset, so if everyone is on board with this plan, the founders We want to support them and make sure they take ownership and that we're all aligned moving forward. To execute a big vision and lead the company to a big exit. ”

Ultimately, the overall risk picture depends on the characteristics of the company and how capital-intensive the business becomes in the future. Also, even if he gets one raise and the company becomes cash flow neutral, which results in healthy organic growth, that's another story. If this continues to be a type of business that is capital intensive and requires multiple rounds of significant financing, the risk profile changes further.

rewind choices

The CEO told me that the company's first investor was a large independent research institute in Norway that often spins out its own companies based on the innovations it develops. . However, in this company's case, the founders made an outside investment on what they now call “below market terms.” The CEO also noted that existing investors on the board had proposed raising capital at a lower valuation. Now he understands that choice could jeopardize the company's long-term success and has regrets. He suspects that venture capitalists don't think his company is investable, and to make sure this issue is front and center for prospective investors, he first explained the reason for including the cap table as a slide in the slide materials.

This problem may not be isolated to this one founder. In many developing startup ecosystems like Norway, good advice can be difficult to come by, and the “norm” is limited to people who don't necessarily understand what the venture model looks like elsewhere. may be determined by.

“I don't want to alienate investors. They're doing a lot of good things, too,” the CEO said.

Unfortunately, Walk said, bad actors aren't as rare as he would like, and Homebrew is not allowing incubators or accelerators to own more than 10% of the stock or own more than 50% of the company on “exploitative terms.” He says that he often encounters situations where he does this. If it has already been sold to an investor, or if the majority of the shares are allocated to fully vested founders who may no longer be in the company.

As a result, non-local investors who want to invest in companies in the early stages of ecosystem development may have great opportunities. They can choose to offer promising early-stage startups more reasonable terms than what local investors are willing to offer. Get the best investment and local investors will compete for scraps. However, the obvious drawback is that this means a significant financial drain from the ecosystem. Instead of keeping money at home, wealth (and potentially talent) flows overseas. The local ecosystem is just like that. I'm trying to avoid it.

==

If you have a news tip or information about Haje, you can share it via email or Signal.